The financial system today is a lot different from the past. Interest rates have been decreasing for 10 years and are now finally starting to increase. There is a whole generation of millennials that only know the age of low interest rates and easy access to credit to finance the things they want in life. Student loans, car loans, furniture and appliance cards, cell phone plans and home purchasing, the average Canadian now spends 1.6 dollars for every dollar they earn, meaning someone with a salary of $45,000 dollars per year on average will purchase $72,000 worth of goods and services via financing. If someone is facing consumer debt, the last things thought about is putting the money away to achieve financial freedom however a few simple strategy shifts can change the trajectory of their financial destiny.

There are a million ways in order start walking on the path to complete financial freedom. Today I will cover some of the most researched strategies set out by some of the worlds greatest investors to help the average person achieve financial freedom.

1) Control your own investments. Get a Self Directed brokerage account at Questrade.com

There are a million ways in order start walking on the path to complete financial freedom. Today I will cover some of the most researched strategies set out by some of the worlds greatest investors to help the average person achieve financial freedom.

1) Control your own investments. Get a Self Directed brokerage account at Questrade.com

As employees and business owners we are already financial traders, trading money for our time which is simply the worst financial trade you can make long term because time is priceless. The most important decision use a portion of your earned income to make money while while sleep. The best way to do do so is to tap into the law of compounding. You can start small and over time the amounts will compound into large sums over time even with average returns. The key is to start while you're young and continue to make deposits over time. A word of caution, Banks, Mutual Funds and Hedge Funds are designed to take as much as the client can bare to part with. In order for them to to make a living, management fees are taken from your account and the fees outweigh the returns. You can reduce this by self directing.

Questrade allows you so sign up online and build your own investing portfolio. You can and make regular deposits into your investment account via online banking or bill pay. The software is quick, efficient , paperless and can easily be accessed on your smart phone so you can invest on the go.

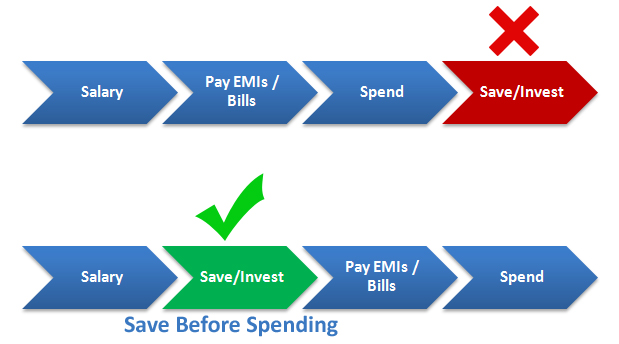

2) Pay yourself first

Questrade allows you so sign up online and build your own investing portfolio. You can and make regular deposits into your investment account via online banking or bill pay. The software is quick, efficient , paperless and can easily be accessed on your smart phone so you can invest on the go.

2) Pay yourself first

When you start to earn money, immediately people tend to go into bill payment mode and have to spend 100% of their income leaving little to no room for savings. The concept of pay yourself first came from a financial adviser who told his clients that if the government were to raise taxes, people would complain but eventually they would adjust and pay the extra tax. By applying a personal tax on yourself to start saving you can start investing immediately. So the fist bill you pay should be to yourself in your financial freedom account and everything else comes after that.

You have two options when setting up a pay yourself first system, you can speak to your HR department at work and get a second deposit account connected or you can set up automatic bill payments every month via online banking. You may start off with a small percentage of saving like 5% and gradually move towards at least 20% of every payment you receive. Having the luxury of cash gives you the opportunity do things like purchase a business for yourself, or property with an income suite to be able to live for fairly cheap.

There is an example of a girl in new york who saved 70% of her income and was able to retire at the age of 28. You can check out her blog here. Deciding to become an owner and invest is the single greatest decision you can make as a young person because in investments time is the greatest asset.

3) Buy the market, vs trying to beat the market picking stocks

You have two options when setting up a pay yourself first system, you can speak to your HR department at work and get a second deposit account connected or you can set up automatic bill payments every month via online banking. You may start off with a small percentage of saving like 5% and gradually move towards at least 20% of every payment you receive. Having the luxury of cash gives you the opportunity do things like purchase a business for yourself, or property with an income suite to be able to live for fairly cheap.

There is an example of a girl in new york who saved 70% of her income and was able to retire at the age of 28. You can check out her blog here. Deciding to become an owner and invest is the single greatest decision you can make as a young person because in investments time is the greatest asset.

3) Buy the market, vs trying to beat the market picking stocks

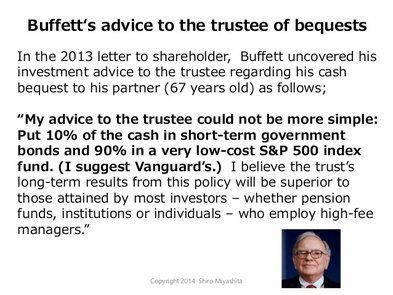

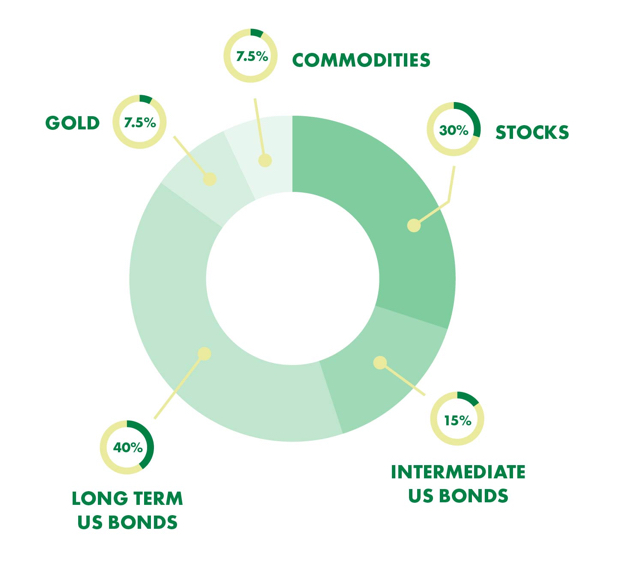

Alot of new investors get confused with what stocks to pick, often if they do not understand the market so they put it off until a later time or put their money in the hands of a bank. As it is said you can never beat the house, so you need to have a strategy of buying a piece of the house itself. The best way to do that would be by using an Exchange Traded Fund or ETF for short. Vanguard is a low fee ETF company that enables investors to buy indexes like the S&P500, top 500 public companies in America. Buy buying the market you do not have to spend countless hours analyzing individual companies. On average the SP500 has returned close to 10% annually over the last 100 years. Warren Buffet, has been very public in the recent years about buying low cost index funds instead of purchasing mutual funds or hedge funds . He advised his wifes trust to use vanguard index funds as the vehicle to buy the market. This is a bet that america will continue to grow and create profitable businesses.

4) Buy right away, time in the market is better than trying to pick the right time

4) Buy right away, time in the market is better than trying to pick the right time

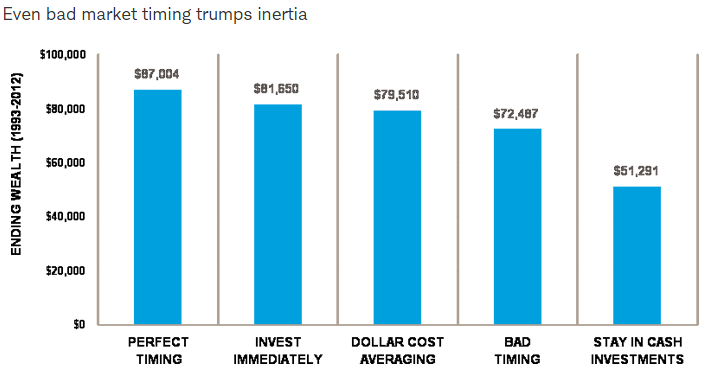

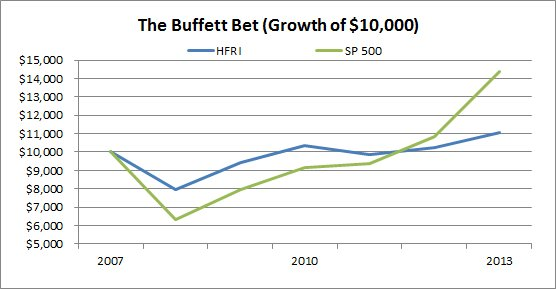

In the study above Each investor received $2,000 at the beginning of every year for the 20 years starting in 1992 and ending in 2012. They left the money in the market, as represented by the S&P 500® Index.

One of the common questions for investors is "is this the right time to invest? should I buy now or wait for a market crash to buy" The answer is simple, even the greatest investors in the world have no idea which direction the market is going to move so so its best to start right away and consistently make purchases of the market over long periods of time vs waiting for the right time. Cash has always been the worst performing asset because inflation makes the purchasing power of cash decrease each year.

Follow these simple strategies and you will put yourself in the right path to financial freedom. See you there.

One of the common questions for investors is "is this the right time to invest? should I buy now or wait for a market crash to buy" The answer is simple, even the greatest investors in the world have no idea which direction the market is going to move so so its best to start right away and consistently make purchases of the market over long periods of time vs waiting for the right time. Cash has always been the worst performing asset because inflation makes the purchasing power of cash decrease each year.

- Peter Perfect was a perfect market timer. He had incredible skill (or luck) and was able to place his $2,000 into the market every year at the lowest monthly close.

- Ashley Action took a simple, consistent approach: Each year, once she received her cash, she invested her $2,000 in the market at the earliest possible moment.

- Matthew Monthly divided his annual $2,000 allotment into 12 equal portions, which he invested at the beginning of each month. This strategy is known as dollar cost averaging.

- Rosie Rotten had incredibly poor timing—or perhaps terribly bad luck: She invested her $2,000 each year at the market's peak, in stark defiance of the investing maxim to "buy low."

- Larry Linger left his money in cash investments (using Treasury bills as a proxy) every year and never got around to investing in stocks at all. He was always convinced that lower stock prices—and, therefore, better opportunities to invest his money—were just around the corner. Refrence: Charles Schwab Study

Follow these simple strategies and you will put yourself in the right path to financial freedom. See you there.

RSS Feed

RSS Feed